1,000+ New Stores, Record Prices, and a Market That Refused to Slow Down

On Akshaya Tritiya 2026, India’s jewellery market delivered more than just strong sales—it delivered a structural signal. Initial industry estimates pegged festive sales at Rs 20,000 crore, up from ~Rs 16,000 crore last year. However, as the day progressed—with packed stores, extended shopping hours, and sustained footfalls across metros and Tier II cities—trade feedback increasingly pointed to actual sales surpassing early projections by a meaningful margin.

What makes this surge particularly significant is the context in which it is unfolding. Gold prices, hovering at Rs 1.55–1.58 lakh per 10 grams, are among the highest ever recorded. Yet, instead of dampening demand, they appear to have reshaped it. The contradiction is stark, but it is also revealing—it signals not a slowdown, but a market that is recalibrating in real time.

A Market Where Value Is Rising Faster Than Volume

Beneath the headline growth, the underlying dynamics present a more nuanced picture. While overall sales value has risen sharply, volumes have remained stable or moderated, reflecting the impact of elevated gold prices. Footfalls, on the other hand, have strengthened further, indicating that consumer intent remains intact even as purchasing patterns evolve.

This divergence between value and volume highlights a critical shift. Consumers are not stepping away from jewellery purchases; instead, they are recalibrating their choices. Spending is increasingly being redistributed toward lower-weight pieces, design-led offerings, and alternative categories such as diamonds, silver, and lab-grown stones. The market, therefore, is not contracting—it is evolving in composition.

This divergence between value and volume highlights a critical shift. Consumers are not stepping away from jewellery purchases; instead, they are recalibrating their choices. Spending is increasingly being redistributed toward lower-weight pieces, design-led offerings, and alternative categories such as diamonds, silver, and lab-grown stones. The market, therefore, is not contracting—it is evolving in composition.

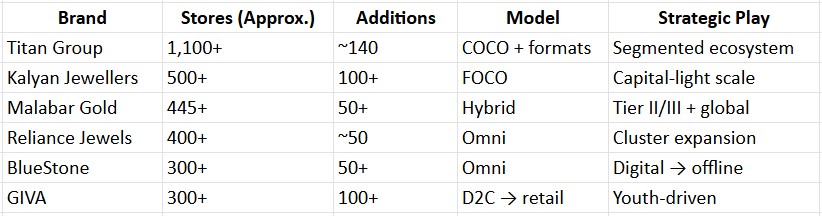

The Big Backdrop: 1,000+ Stores Added Before the Festival

If demand tells one side of the story, supply tells another—far more aggressive one. Over the past 12 to 18 months, the Indian jewellery industry has added more than 1,000 stores across formats and geographies. This expansion spans national chains such as Titan (Tanishq, Mia, CaratLane), Kalyan Jewellers, Malabar Gold & Diamonds, and Reliance Jewels; mid-sized players like Candere, Indriya, Kisna, ORRA, PNG, and Senco; as well as strong regional players including GRT, Bhima, Lalithaa, and TBZ. Alongside them, a new wave of digital-first brands such as GIVA, BlueStone, Limelight, and Jewelbox has rapidly built offline presence.

This level of expansion is unprecedented in the category. More importantly, it signals a deeper shift: the industry is no longer expanding in response to demand alone; it is proactively building retail capacity in anticipation of future consumption. In effect, supply is beginning to lead demand.

This level of expansion is unprecedented in the category. More importantly, it signals a deeper shift: the industry is no longer expanding in response to demand alone; it is proactively building retail capacity in anticipation of future consumption. In effect, supply is beginning to lead demand.

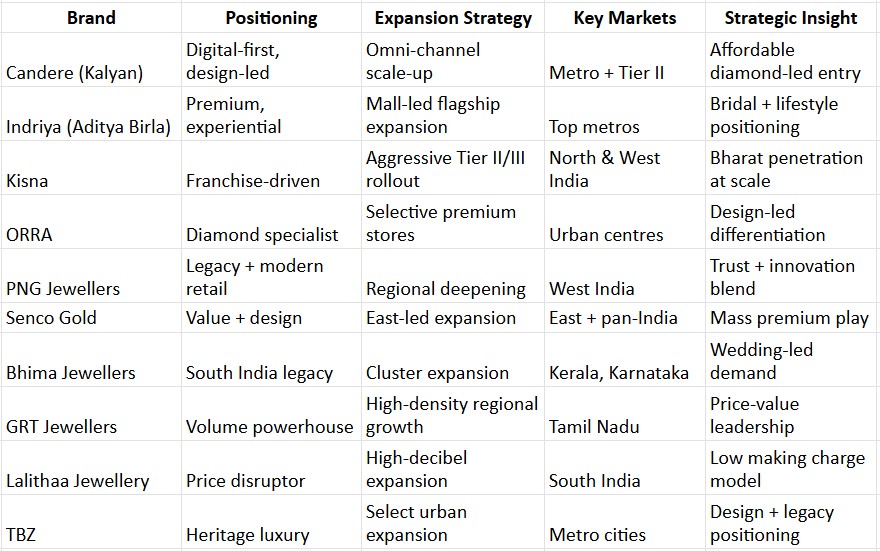

This expansion is not being driven by large national players alone. A strong layer of mid-sized and regional chains is adding depth to the market, particularly across Tier II and III cities.

Mid-Sized & Emerging Jewellery Chains – Expansion Momentum (FY25–FY26)

Mid-sized and regional players are no longer peripheral—they are driving depth in the market. While national chains build scale, these brands are capturing local trust, wedding demand, and value-conscious consumers, especially in Tier II and III cities. Their expansion is often more aggressive in terms of pricing and promotions, making them critical to understanding real demand beyond metros.

Mid-sized and regional players are no longer peripheral—they are driving depth in the market. While national chains build scale, these brands are capturing local trust, wedding demand, and value-conscious consumers, especially in Tier II and III cities. Their expansion is often more aggressive in terms of pricing and promotions, making them critical to understanding real demand beyond metros.

Malls Emerge as the New Centre of Gravity

A defining feature of this expansion cycle is its concentration within organised retail environments, particularly malls. These spaces are increasingly becoming the primary interface between brands and consumers, offering a combination of trust, visibility, and experiential engagement that traditional formats struggle to replicate.

At Nexus Elante Mall in Chandigarh, the Jewel Souk concept exemplifies this shift. By bringing together leading brands such as Tanishq, Malabar Gold & Diamonds, CaratLane, Reliance Jewels, and Indriya into a single curated zone, the mall has effectively created a modern jewellery marketplace within a controlled retail environment.

| Element | Impact on Consumer Behaviour |

|---|---|

| Multi-brand clustering | Enables comparison-led buying |

| High visibility | Drives discovery and impulse |

| Festive campaigns | Increases dwell time |

| Extended hours | Converts intent into purchase |

Within this ecosystem, brands layered their individual campaigns—ranging from steep making charge discounts to gold rate protection schemes and bridal-focused experiences. The result has been a noticeable shift in consumer behaviour, from single-store transactions to multi-brand exploration, and from planned purchases to experience-led discovery. Malls, in this context, are no longer just retail venues; they are becoming active facilitators of jewellery consumption.

Demand Is Not Weak—It Is Being Rewired

Industry sentiment reinforces the idea that demand has not weakened—it has evolved. Retailers consistently point to a more intentional, value-conscious, and design-driven consumer. Buying decisions are increasingly influenced by practicality and versatility, with a clear preference for jewellery that can be worn frequently rather than stored for occasional use.

| Industry Insight | What It Means |

|---|---|

| Considered choice over ritual | Shift to intent-led buying |

| Practical, wearable value | Rise of everyday jewellery |

| Demand evolves, doesn’t disappear | Redistribution across categories |

Even emerging segments such as men’s jewellery—particularly chains and bracelets—are gaining traction, indicating a broadening of the consumer base and a gradual normalisation of jewellery as an everyday category across demographics.

The Festival Has Evolved into a Retail Event

Akshaya Tritiya itself is undergoing a transformation. What was once a largely cultural and ritual-driven buying occasion has now evolved into a fully orchestrated retail cycle. Brands across the spectrum—ranging from large national chains to regional players and lab-grown diamond specialists—have aligned around a common strategy: reducing friction and increasing conversion.

This has been achieved through a combination of pre-booking schemes, price protection offers, making charge waivers, cashback incentives, and exchange benefits. Together, these mechanisms have reshaped the buying journey, making it more flexible, less risky, and more appealing in a high-price environment.

As a result, Akshaya Tritiya 2026 reveals a market that is not slowing down, but shifting gears. Value growth continues to outpace volume, retail expansion is running ahead of demand, and consumption is becoming more fragmented yet more frequent. Most importantly, the industry is no longer waiting for demand to emerge—it is actively engineering it.

THE GREAT INDIAN JEWELLERY RESET

From Gold Buying to Jewellery Consumption

If the scale of expansion defines the market externally, the real transformation is unfolding within the consumer. The traditional jewellery buyer—largely driven by occasions, family decisions, and gold as a store of value—is gradually being complemented by a more diverse and dynamic set of consumers. Working women are increasingly driving self-purchase, Gen Z is entering the category through accessible formats such as silver, 14K gold and lab-grown diamonds, and consumers in Tier II and III cities are upgrading from unorganised to branded retail environments. Even segments that were historically under-penetrated, such as men’s jewellery, are beginning to show meaningful traction.

This diversification is critical to sustaining growth in a high-price environment. It ensures that demand is no longer dependent on a single buying cycle or consumer type. Instead, it is being distributed across multiple occasions, use cases, and price points. Jewellery, in this context, is steadily transitioning from an inheritance-led category to one that is driven by identity, self-expression, and everyday relevance.

18K and 14K: Redefining the Economics of Jewellery Buying

The clearest manifestation of this shift is the rapid rise of 18-carat and 14-carat gold formats. Once positioned as alternatives to traditional 22K jewellery, these formats are now moving to the centre of consumption, driven by both affordability and functionality.

| Gold Purity | Purity % | Rate per Gram | Consumer Implication |

|---|---|---|---|

| 22K | 91.6% | ₹13,900–14,300 | Traditional, high-cost |

| 18K | 75% | ₹11,400–11,700 | Aspirational middle |

| 14K | 58.5% | ₹8,900–9,100 | Affordable entry |

The pricing differential is substantial enough to influence behaviour at scale. For a typical 10-gram purchase, the savings between 18K and 14K can approach ₹30,000, fundamentally altering purchase decisions. What emerges from this is not a decline in demand, but a recalibration of how value is optimised. Consumers are effectively managing rising prices by adjusting purity levels, without stepping away from the category altogether.

| Weight | 18K Price (Approx.) | 14K Price (Approx.) | Savings |

|---|---|---|---|

| 1 gram | ~Rs 13,300 | ~Rs 10,400 | ~Rs 3,000 |

| 5 grams | ~Rs 66,000 | ~Rs 52,000 | ~Rs 14,000 |

| 10 grams | ~Rs 1.33 lakh | ~Rs 1.04 lakh | ~Rs 30,000 |

This economic logic is further reinforced by product functionality. Lower-carat gold is more durable, better suited for daily wear, and structurally more compatible with diamond and gemstone settings. As a result, it aligns seamlessly with contemporary design sensibilities and evolving usage patterns.

The Rise of ‘Lived-In Luxury’

The shift in purity is closely linked to a broader change in how jewellery is perceived and used. Increasingly, jewellery is being designed and purchased not as a static asset, but as something to be worn regularly. This has given rise to what can best be described as ‘lived-in luxury’—pieces that balance aspiration with practicality.

Across brands, demand is strongest for lightweight, versatile designs such as minimalist studs, stackable bracelets, delicate chains, and personalised pendants. These products are not tied to specific occasions; instead, they integrate into daily wardrobes, encouraging more frequent usage and, by extension, more frequent purchase cycles. The emphasis is shifting from ownership to usability, and from occasional indulgence to everyday relevance.

Diamonds and Lab-Grown Alternatives: Expanding the Consumption Base

Parallel to the evolution in gold formats is the growing traction of diamonds, particularly lab-grown diamonds. While natural diamonds continue to hold aspirational value, lab-grown alternatives are expanding the category by lowering the entry barrier.

| Parameter | Natural Diamonds | Lab-Grown Diamonds |

|---|---|---|

| Price | Premium | Significantly lower |

| Accessibility | Limited | Wider |

| Consumer Base | Traditional | Younger, first-time buyers |

| Use Case | Bridal | Everyday and gifting |

Brands operating in the lab-grown segment are not merely competing on price; they are redefining value by offering larger stones, contemporary designs, and strong buyback assurances. This combination allows them to attract a new cohort of consumers who might otherwise have deferred or avoided diamond purchases altogether. In doing so, they are adding incremental demand rather than redistributing existing demand.

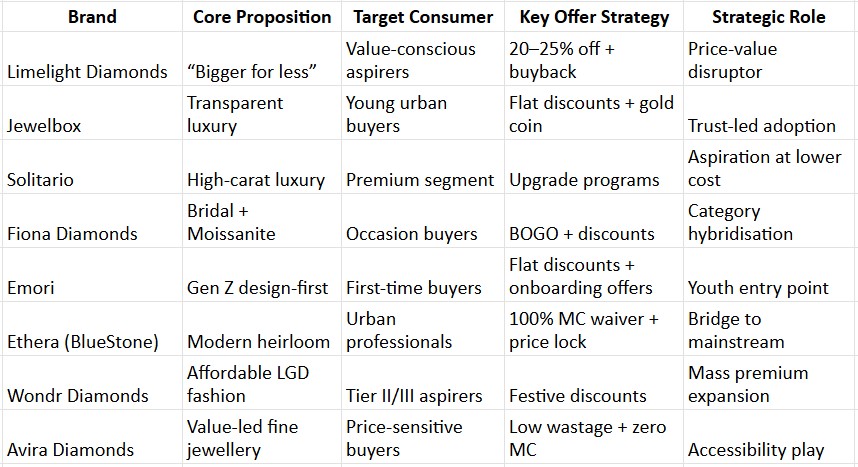

A new set of specialised players is leading this shift, each targeting distinct consumer segments and use cases.

Lab-Grown Diamond (LGD) Brands – The New Demand Creators

LGD players are not just competing with traditional jewellers—they are expanding the category itself. By combining lower prices, strong design appeal, and buyback assurances of up to 80–90%, they are addressing both affordability and trust. Their real impact lies in bringing first-time buyers into the diamond category, especially younger consumers who may not have participated otherwise.

LGD players are not just competing with traditional jewellers—they are expanding the category itself. By combining lower prices, strong design appeal, and buyback assurances of up to 80–90%, they are addressing both affordability and trust. Their real impact lies in bringing first-time buyers into the diamond category, especially younger consumers who may not have participated otherwise.

Smart Buying as the New Consumer Behaviour

Taken together, these shifts point to a new pattern of behaviour that can best be described as “smart buying.” Consumers are no longer making jewellery purchases purely on sentiment or tradition. Instead, they are evaluating multiple variables—price, purity, design, resale value, and flexibility—before making decisions. This includes pre-booking gold rates, choosing lower-carat formats, opting for lighter designs, and comparing offerings across brands and channels.

The cumulative effect is a market that is becoming more rational, more segmented, and more responsive to economic realities. Jewellery is no longer defined solely by what it represents symbolically; it is increasingly defined by how effectively it fits into the consumer’s lifestyle and financial framework.

The transformation underway is structural rather than cyclical. Consumers are not exiting the category—they are reshaping it through their choices. As jewellery becomes more wearable, more accessible, and more aligned with everyday life, its role within the consumption basket is expanding. The shift from gold buying to jewellery consumption is no longer an emerging trend; it is becoming the defining characteristic of the market.

Engineering Demand and Redefining Trust

If consumer behaviour explains why demand has held up, brand strategy explains how it has been converted into sales at scale. Akshaya Tritiya 2026 was not driven by passive demand; it was actively shaped through a combination of pricing innovation, promotional engineering, and trust-building mechanisms that collectively reduced friction in the buying process.

From Promotional Offers to Structured Value Creation

Across the industry, brands moved beyond traditional discounting to introduce more sophisticated value propositions. Gold rate protection schemes allowed consumers to lock in prices with minimal upfront commitment, effectively shielding them from volatility. Making charge waivers and cashback incentives reduced the perceived cost of purchase, while bundled benefits such as free coins and vouchers enhanced the overall value proposition.

| Strategy | Consumer Benefit | Market Impact |

|---|---|---|

| Gold Rate Protection | Price certainty | Encourages early commitment |

| Making Charge Waivers | Lower upfront cost | Improves conversion |

| Cashback & Vouchers | Added value | Enhances perceived savings |

| Free Coins | Emotional + financial incentive | Drives ticket size |

| Exchange Benefits | Easier upgrades | Increases repeat purchase |

These mechanisms worked in tandem to address the key barriers to purchase in a high-price environment. Instead of waiting for prices to stabilise, brands created conditions under which consumers felt confident proceeding with their purchases.

Buyback and Exchange: The New Trust Infrastructure

Perhaps the most significant evolution has been in the area of buyback and exchange policies. Leading brands have standardised frameworks that offer full value on exchanges within the same brand and high buyback percentages, effectively turning jewellery into a more liquid and flexible asset.

| Brand | Exchange Value | Buyback Value | Key Shift |

|---|---|---|---|

| Tanishq | 100% | ~90% | Multi-carat flexibility |

| CaratLane | 100% | ~90% | Seamless upgrades |

| Malabar Gold | 100% | Assured | Cross-brand acceptance |

| BlueStone | 100%+ | 90–100% | Incentivised exchange |

This shift fundamentally changes the nature of jewellery ownership. Purchases are no longer seen as final decisions but as part of an ongoing cycle of upgrade and exchange. The perceived risk associated with high-value buying is significantly reduced, making consumers more willing to transact even at elevated price levels.

Risk Reduction as a Demand Driver

At current price levels, the biggest barrier to purchase is not affordability alone, but hesitation. Brands have responded by systematically addressing this hesitation through structured interventions—price locks to manage volatility, exchange options to provide flexibility, and buyback guarantees to ensure value retention.

| Consumer Concern | Industry Response |

|---|---|

| Price volatility | Rate lock schemes |

| High upfront cost | Discounts and waivers |

| Post-purchase regret | Easy exchange policies |

| Value retention | Buyback guarantees |

By removing uncertainty at multiple points in the buying journey, the industry has effectively converted intent into action. Jewellery buying, once characterised by high commitment, is becoming increasingly fluid and reversible.

Competitive Intensity and Market Maturity

The combination of rapid store expansion and aggressive promotional strategies has intensified competition across the sector. Consumers today have access to a wide array of brands, formats, and price points, making differentiation more challenging. In this environment, success is increasingly determined by a brand’s ability to integrate product design, pricing strategy, customer experience, and trust mechanisms into a cohesive offering.

The market is, therefore, moving toward a more mature and competitive equilibrium, where scale alone is insufficient and value creation becomes the primary differentiator.

Beyond the Gold Rush

Akshaya Tritiya 2026 marks a defining moment for the Indian jewellery industry. It reflects a market that is expanding ahead of demand maturity, diversifying across categories, and adapting rapidly to changing consumer expectations. The convergence of retail expansion, product innovation, and financial structuring has created a new growth model—one that is less dependent on traditional triggers and more aligned with contemporary consumption patterns.

At its core, the shift is unmistakable. India is moving away from a purely gold-centric, savings-driven approach toward a broader jewellery consumption ecosystem. In this new paradigm, value is defined not just by purity or weight, but by design, usability, flexibility, and relevance to everyday life.

The crowds seen this Akshaya Tritiya tell one story, and the data tells another. Together, they point to a deeper transformation.

India is not just buying more jewellery—it is redefining how jewellery is bought, worn, and valued.