India’s ₹8.3 Lakh Crore Jewellery Market Is Entering a New Era Where the Strongest Brands Are No Longer Just Selling Gold — They Are Building Complete Consumption Ecosystems

India’s jewellery industry is entering one of the most strategically important transitions in its history.

After completing one of the biggest physical expansion cycles ever witnessed in Indian retail, the sector is now confronting a dramatically altered growth environment shaped by record gold prices, rising import duties, changing consumer behaviour, premium retail rentals and recalibrating discretionary spending patterns. Yet, beneath these immediate pressures lies a much larger structural transformation story that could redefine the future of organised jewellery retail in India.

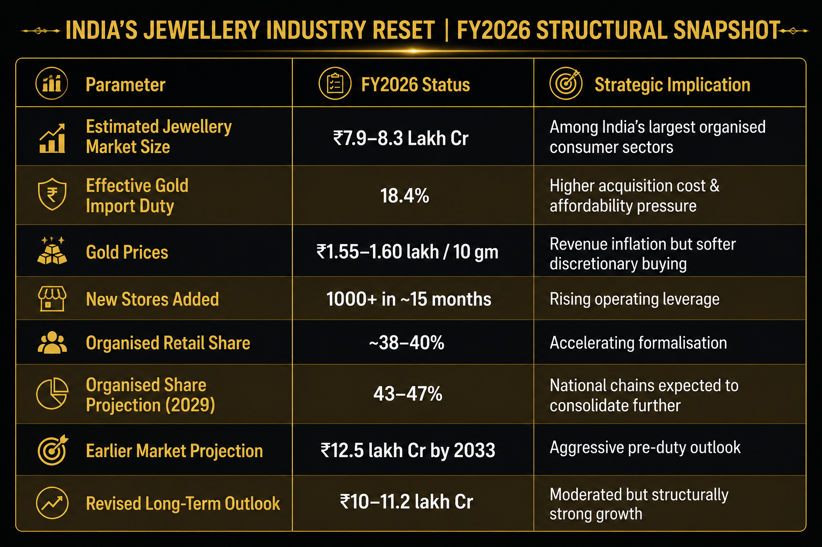

The country’s jewellery market, now estimated at nearly ₹7.9–8.3 lakh crore ($95–100 billion) in FY2025–26, is no longer evolving merely as a bullion-led business centred around weddings and investment purchases. Increasingly, India’s strongest jewellery companies are transforming themselves into integrated lifestyle ecosystems spanning fashion, textiles, hypermarkets, malls, hospitality, fragrances, omni-channel commerce, beauty, gifting and Gen-Z lifestyle categories.

This strategic shift became even more important in May 2026, when the government raised the effective import duty on gold to nearly 18.4%, intensifying pressure on already elevated gold prices hovering around ₹1.55–1.60 lakh per 10 grams in several markets. Simultaneously, Prime Minister Narendra Modi’s public appeal urging citizens to avoid unnecessary gold purchases for a year introduced a new psychological and behavioural dimension into the market.

The immediate response was visible across Dalal Street, where jewellery-linked stocks corrected sharply as investors reassessed growth assumptions for one of India’s most aggressively expanding retail categories. But beyond the market reaction lies a much larger question:

Can jewellery businesses dependent primarily on bullion-driven growth sustain long-term expansion in an environment where gold prices, rentals and operating costs continue rising simultaneously?

India’s leading jewellery groups increasingly appear to have found the answer: Expand beyond gold

One of the most important strategic lessons emerging from the current phase is that jewellery retail alone may no longer be sufficient to sustain long-term growth at scale.

One of the most important strategic lessons emerging from the current phase is that jewellery retail alone may no longer be sufficient to sustain long-term growth at scale.

Historically, jewellery businesses depended heavily on weddings, festive demand and investment buying. Today, the most future-ready players are increasingly using adjacent lifestyle categories to generate recurring engagement, diversify margins and reduce vulnerability to bullion volatility. Fashion, textiles, fragrances, beauty, eyewear, hypermarkets and hospitality are increasingly becoming strategic balancing engines capable of stabilising consumer engagement even during periods of softer gold demand.

This transition is particularly significant because jewellery retail often operates on relatively thin making-charge margins, while categories such as fashion, ethnic wear and beauty frequently generate significantly higher operating profitability alongside faster inventory rotation and more frequent purchase cycles.

The result is a gradual but powerful transformation:

India’s jewellery retailers are increasingly becoming lifestyle ecosystem companies.

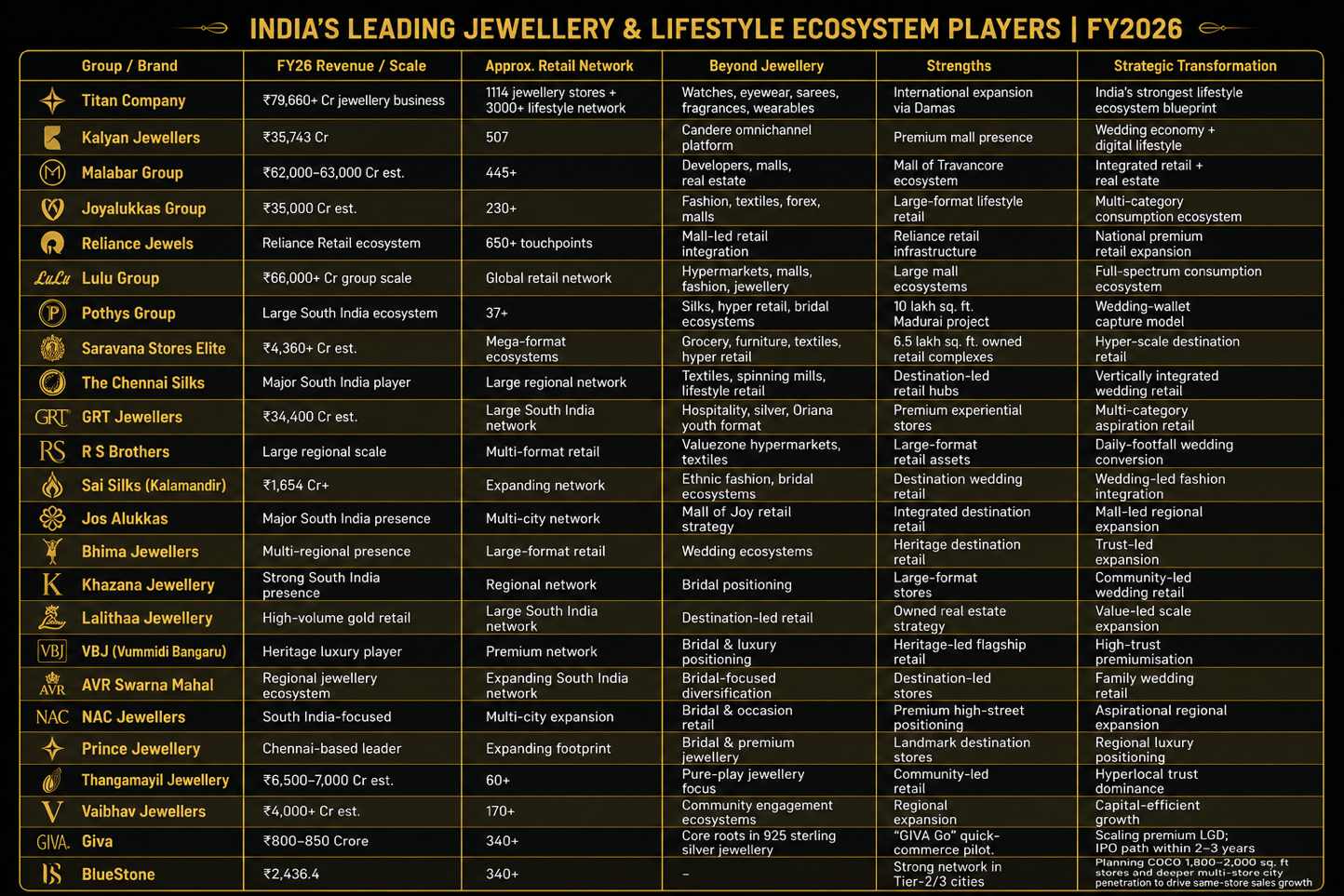

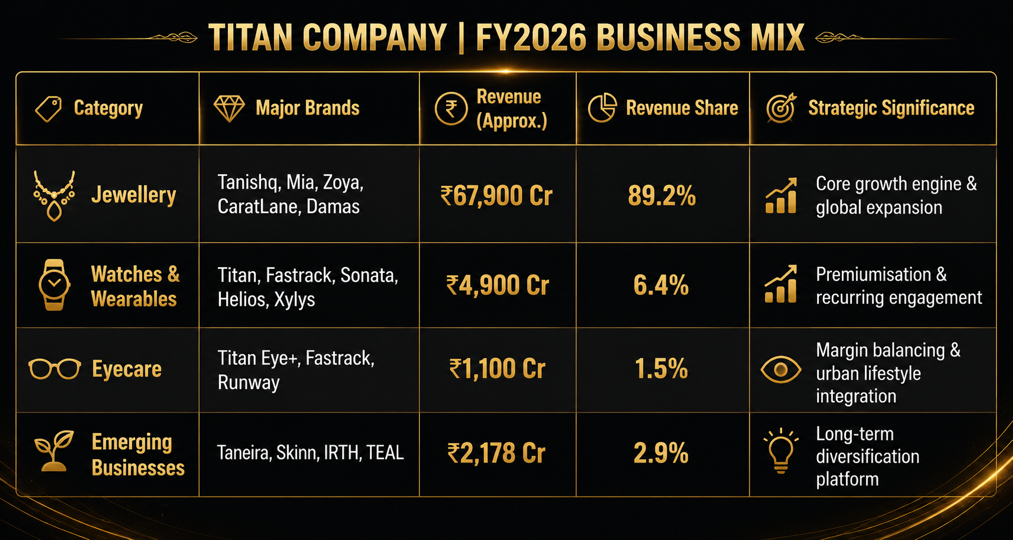

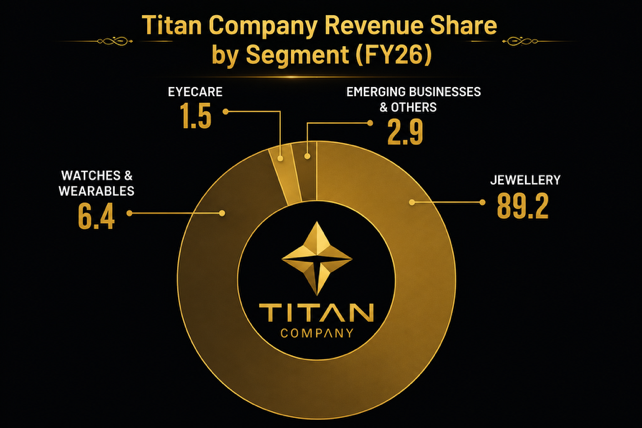

Among organised retail corporates, Titan Company remains perhaps the clearest example of how India’s jewellery industry can evolve beyond bullion into a broader lifestyle ecosystem. Based on FY26 consolidated results ending March 31, 2026, Titan reported total income of nearly ₹76,078 crore excluding bullion and digi-gold sales. Jewellery contributed almost 89.2% of total revenues through brands such as Tanishq, Mia, Zoya, CaratLane and Damas. However, the larger strategic significance lies in the company’s steadily expanding non-jewellery ecosystem spanning watches, wearables, eyewear, sarees, fragrances

Among organised retail corporates, Titan Company remains perhaps the clearest example of how India’s jewellery industry can evolve beyond bullion into a broader lifestyle ecosystem. Based on FY26 consolidated results ending March 31, 2026, Titan reported total income of nearly ₹76,078 crore excluding bullion and digi-gold sales. Jewellery contributed almost 89.2% of total revenues through brands such as Tanishq, Mia, Zoya, CaratLane and Damas. However, the larger strategic significance lies in the company’s steadily expanding non-jewellery ecosystem spanning watches, wearables, eyewear, sarees, fragrances  and emerging consumer businesses.Titan’s evolution demonstrates one of the most important strategic lessons emerging across India’s jewellery industry:the future may belong not merely to companies selling gold, but to those building diversified lifestyle ecosystems around trust, aspiration and recurring consumer engagement.

and emerging consumer businesses.Titan’s evolution demonstrates one of the most important strategic lessons emerging across India’s jewellery industry:the future may belong not merely to companies selling gold, but to those building diversified lifestyle ecosystems around trust, aspiration and recurring consumer engagement.

Perhaps the most fascinating transformation is unfolding across South India, where jewellery-led family enterprises have quietly built some of India’s most powerful integrated retail ecosystems. Unlike boutique-led jewellery chains dominant in many North and West Indian markets, several South Indian groups operate gigantic destination-led retail complexes spanning anywhere between 5 lakh sq. ft. and 10 lakh sq. ft., where jewellery, bridal silks, hypermarkets, gifting, furniture, beauty and fashion coexist within a single ecosystem.

The logic is deeply strategic.

A bridal customer shopping for silk sarees naturally becomes a jewellery customer. Hypermarkets sustain daily footfalls. Fashion retail creates recurring engagement. Jewellery acts as the aspirational anchor around which the larger ecosystem functions.

The result is a business model capable of capturing nearly the entire “family lifestyle wallet.”

Pothys is developing a massive 10 lakh sq. ft. integrated retail destination in Madurai after establishing its landmark 5 lakh sq. ft. flagship in Chennai. Saravana Stores has created one of India’s most extraordinary consumption ecosystems integrating jewellery, furniture, grocery, fashion and hyper retail inside gigantic owned retail assets. The Chennai Silks ecosystem similarly combines textiles and jewellery into vertically integrated wedding-led consumption platforms. R S Brothers has built a powerful hybrid model through its Valuezone hypermarket ecosystem, where daily-needs traffic ultimately converts into wedding and jewellery purchases during festive cycles.

One of the biggest strategic advantages these ecosystems enjoy is ownership of real estate. Unlike national chains operating inside premium Grade-A malls with escalating rentals, many South Indian retail groups own their destination retail assets. This significantly reduces occupancy pressure while creating long-term strategic flexibility.

Increasingly, the industry is witnessing a shift: from “gold retail” to “lifestyle ecosystem retail.”

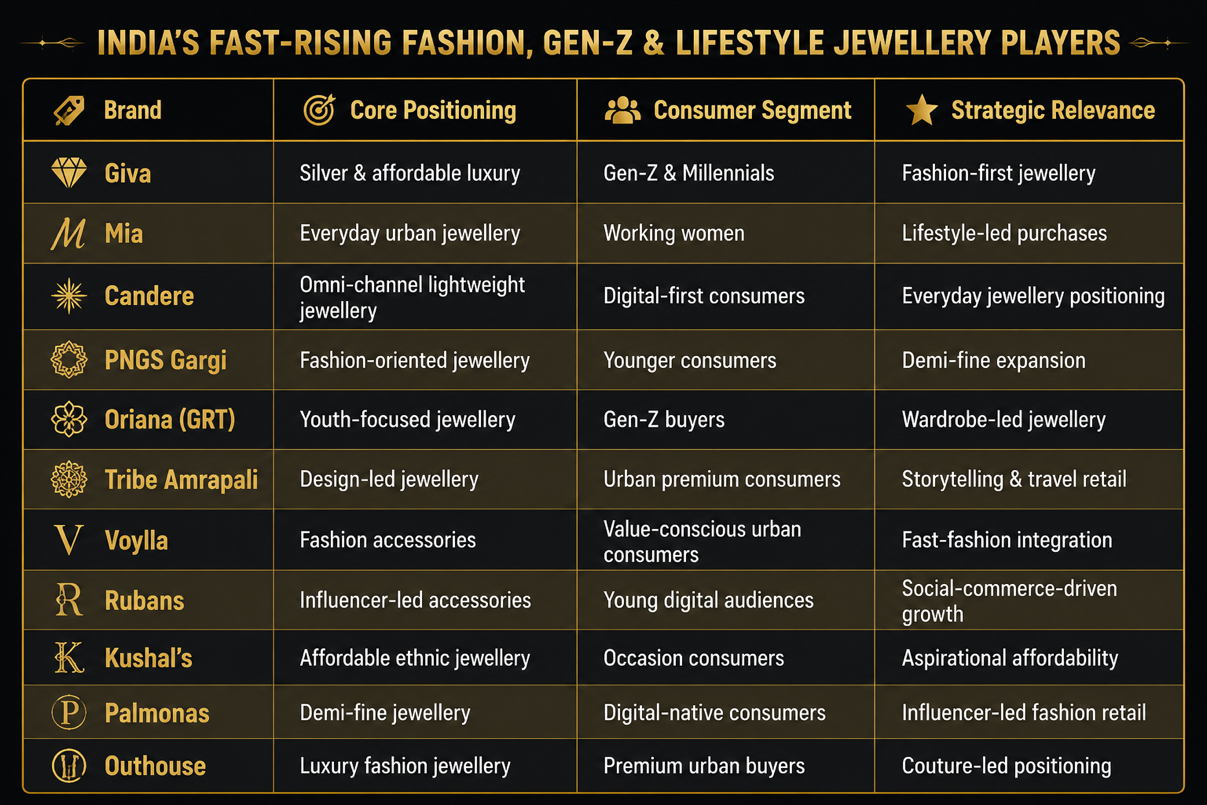

India’s jewellery market is simultaneously witnessing one of its biggest behavioural transitions as younger consumers increasingly treat jewellery less as locker-bound wealth accumulation and more as part of everyday styling, gifting, occasion dressing and self-expression. Growth is accelerating across lightweight jewellery, silver, demi-fine collections and affordable luxury categories that behave far more like fashion retail than traditional investment buying.

India’s jewellery market is simultaneously witnessing one of its biggest behavioural transitions as younger consumers increasingly treat jewellery less as locker-bound wealth accumulation and more as part of everyday styling, gifting, occasion dressing and self-expression. Growth is accelerating across lightweight jewellery, silver, demi-fine collections and affordable luxury categories that behave far more like fashion retail than traditional investment buying.

This behavioural shift is opening entirely new possibilities for organised jewellers to expand into adjacent lifestyle categories while creating more recurring consumer engagement cycles.

This behavioural shift is opening entirely new possibilities for organised jewellers to expand into adjacent lifestyle categories while creating more recurring consumer engagement cycles.

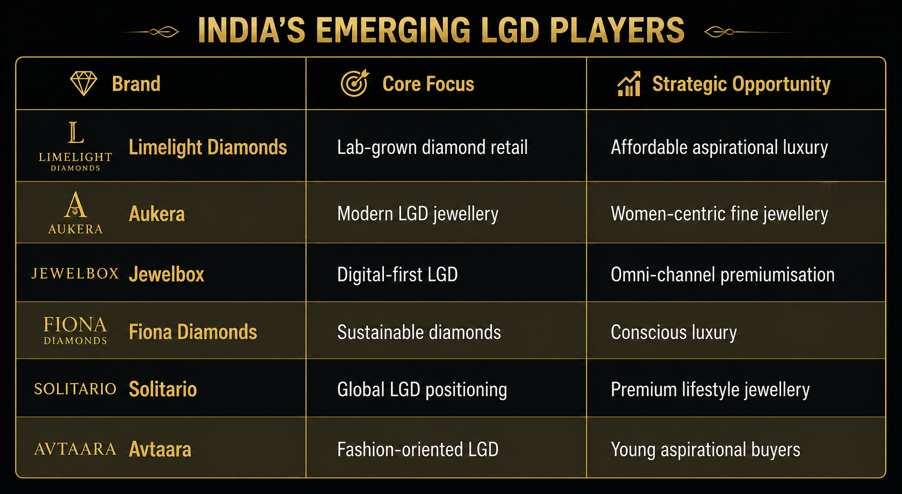

Lab-Grown Diamonds are emerging as another important strategic layer within this transition. Unlike natural diamonds that depend heavily on imported rough stones, LGDs are increasingly being manufactured within India, especially in Surat, while offering significantly lower entry price points for aspirational consumers.

The next phase of India’s jewellery industry may therefore belong not merely to brands selling the most gold —

but to companies capable of building the strongest lifestyle ecosystems around aspiration, weddings, fashion, trust and recurring consumer engagement.